Updates on Rental Relief Framework

Expanded Powers for Rental Relief Assessors

Under the rental relief framework, a landlord who is unable to reach an agreement with is tenant may apply to have an independent rental relief ascertain:

a) The tenant’s eligibility for rental waivers (either the portion supported by Government assistance, and/or the portion borne by the landlord)

b) The landlord’s eligibility to provide a reduced amount of rental waivers, on the basis of financial hardship

The amendments to the Act proposed on September 3, will expand the powers of rental relief assessors so that they can make determinations on unresolved disputes relating to the amount of rent to be waived under the framework, where the amount is affected by any of the following factors:

a) The amount of maintenance and service charges, especially where such charges are not explicitly listed in the lease or license agreement

b) The amount that can be offset by assistance provided by the landlord earlier

c) The tenant is occupying the property for only a part of the relief period

d) There are multiple-sub tenants in the same property

Clarifying Interaction Between Part 8 and Other Dispute Resolution Proceedings

The amendment Bill will also clarify the existing Part 8 of the Act – not yet in force – that allows parties of some contracts to get relief if they are affected by breaches or delays in construction, supply or related contracts.

It will specify that no application for relief for such contracts can be filed if court, arbitral or Building and Construction Industry Security of Payment Act (Sopa) proceedings related to the application have already started.

Conversely, once an application for relief ha been filed, the other parties of the contract cannot commence, arbitral or Sopa proceedings or the same matter, until a determination is made or the application is rejected or withdraw.

If a determination is made and the terms of the contract are adjusted, any subsequent applications and determinations made under Sopa must be based on the adjusted contract terms.

In cases where a Sopa application is made before the other party seeks relief under the Act, the Sopa adjudicator will have powers to grant relief – similar to that of the assessors – to account for the impact of Covid-19.

Updates on Rental Relief Framework

Expanded powers for rental relief assessors

Under the rental relief framework, a landlord who is unable to reach an agreement with is tenant may apply to have an independent rental relief ascertain:

a) The tenant’s eligibility for rental waivers (either the portion supported by Government assistance, and/or the portion borne by the landlord)

b) The landlord’s eligibility to provide a reduced amount of rental waivers, on the basis of financial hardship

The amendments to the Act proposed on September 3, will expand the powers of rental relief assessors so that they can make determinations on unresolved disputes relating to the amount of rent to be waived under the framework, where the amount is affected by any of the following factors:

a) The amount of maintenance and service charges, especially where such charges are not explicitly listed in the lease or license agreement

b) The amount that can be offset by assistance provided by the landlord earlier

c) The tenant is occupying the property for only a part of the relief period

d) There are multiple-sub tenants in the same property

Clarifying interaction between Part 8 and other dispute resolution proceedings

The amendment Bill will also clarify the existing Part 8 of the Act – not yet in force – that allows parties of some contracts to get relief if they are affected by breaches or delays in construction, supply or related contracts.

It will specify that no application for relief for such contracts can be filed if court, arbitral or Building and Construction Industry Security of Payment Act (Sopa) proceedings related to the application have already started.

Conversely, once an application for relief ha been filed, the other parties of the contract cannot commence, arbitral or Sopa proceedings or the same matter, until a determination is made or the application is rejected or withdraw.

If a determination is made and the terms of the contract are adjusted, any subsequent applications and determinations made under Sopa must be based on the adjusted contract terms.

In cases where a Sopa application is made before the other party seeks relief under the Act, the Sopa adjudicator will have powers to grant relief – similar to that of the assessors – to account for the impact of Covid-19.

FAQs on Rental Relief and Property Tax Rebate for SMEs

Rental Relief

What are the eligibility criteria for an SME tenant to qualify for the rental relief?

The rental relief framework, comprising the Rental Relief and the Additional Rental Relief, applies to eligible tenant-occupiers of prescribed properties in qualifying leases or licences that are in writing, or evidenced in writing, which are:

a) (i) Entered into before 25 March 2020; or (ii) entered into before 25 March 2020 but expired and renewed either automatically or in exercise of a right of renewal in the contract; and

b) In force at any time between 1 April and 31 July 2020 for qualifying commercial properties, and between 1 April and 31 May 2020 for other non-residential (e.g. industrial/office) properties.

Rental Relief

Tenant-occupiers must fall in the following category to be eligible for Rental Relief:

a) Small and Medium Enterprises (SMEs) with not more than S$100 million in annual revenue for the Financial Year 2018 or a later appropriate period where applicable, at the individual or entity level

- If the tenant-occupier has not carried on business for 12 months or longer as at the last day of its financial year ending on a date in the year 2018, but has carried on business for 12 months or longer as at last day of its financial year ending on a date in the year 2019, the reference period will be FY2019 instead. Id the foregoing does not apply, but the tenant-occupier has carried on business for 12 months or longer as at the last day of its financial year ending on a date in the year 2020, where the date is on or before March 2020, the reference period will be FY 2020. For any other case, the tenant-occupier’s average monthly revenue from the time the tenant-occupier commenced business until 31 March 2020 (both dates inclusive) will be extrapolated for comparison against the $100 million annual revenue threshold.

Additional Rental Relief

The Additional Rental Relief will apply to tenant-occupiers who qualify for Rental Relief, have carried on business at the rented property before 25 March 2020 and meet the following additional criteria:

(a) The tenant-occupier is a company/entity incorporated in Singapore, and if it is a member of a Singapore group of entities during the period 1 Apr 2020 to 31 May 2020, the aggregate revenue for such a group is not more than S$100 million for the Financial Year 2018 or a later appropriate period where applicable; and

(b) The tenant-occupier suffered at least a 35% drop in average monthly gross income at the outlet level from 1 Apr to 31 May 2019, or alternative period if the tenant-occupier was not operational as of 1 Apr 2019.

Note: If the tenant-occupier commenced business after 1 Apr 2019, comparison will be against the period from the date of commencement of business to 24 Mar 2020 (both dates inclusive) to ascertain the decrease of 35% or more.

How many months of rental relief can an eligible SME tenant (including sub-tenants, licensees and sub-licensees) obtain?

a) Rental Relief for eligible SME tenants (supported by Government assistance):

Eligible tenant-occupiers in qualifying commercial properties and other non-residential properties will receive the rental relief through a waiver of rent from their landlords. Property owners will receive support through the: (a) Property Tax Rebate for Year 2020 announced in the Unity and Resilience Budgets; and (b) Government cash grant announced in the Fortitude Budget.

Eligible SMEs in qualifying commercial properties will receive up to 2 months’ waiver of their rent, and eligible SMEs in other non-residential properties (e.g. industrial and office properties) will receive up to 1 months’ waiver of their rent.

b) Additional Rental Relief for SME tenants (supported by landlords/ property owners):

Eligible SME tenant-occupiers who have seen a 35% or more drop in their average monthly gross income due to COVID-19 will receive up to an additional 2 months’ waiver of rent for qualifying commercial properties, and up to an additional 1 month’s waiver of rent for other non-residential properties (e.g. industrial and office properties).

For more details on the definitions of property in each category, please refer to this.

*The value of the rent to be waived is based on the contractual rent of the tenant, excluding any maintenance fee and charges for the provision of services such as cleaning and security.

What happens if the rent which an intermediary landlord collects from his tenant is higher than the rent he pays to his landlord? Will he be required to absorb the difference in granting the rental waivers?

An intermediary landlord will be required to provide a full waiver to their tenant according to the applicable rental relief period.

What if a company is newly incorporated and does not have financial statements for the financial year 2018 or 2019?

- In such a case, the tenant-occupier should provide its unaudited balance-sheet, profit and loss statement and cash flow statement for the period from the date of commencement of the business (at the prescribed property or any other place) to 31 March 2020 (both dates inclusive), supported by a statutory declaration by the tenant or (if the tenant is an entity) a relevant officer of the tenant.

- If however, the above is also not available, the tenant should provide a statutory declaration by the tenant or (if the tenant is an entity) a relevant officer of the tenant stating that the revenue of the tenant, calculated using the formula 12xA is not more than $100 million, where A is the average monthly revenue from the business for the period from the date of commencement of the tenant’s business to 31 March 2020 (both dates inclusive).

- A statutory declaration made in Singapore must be in the form set out in the First Schedule of the Oaths and Declarations Act (Cap. 211) and be made before a Commissioner for Oaths.

Can a landlord take enforcement action against tenants for non-payment of rent pending IRAS’ notice of cash grant?

The Act provides for a moratorium on enforcement actions against eligible tenant-occupiers for non-payment of rent. Among other things, landlords are prohibited from taking the following actions on the tenant-occupier or the tenant-occupier’s guarantor/surety in relation to the non-payment of rent:

a) Terminating the lease or licence agreement;

b) Exercising the landlord’s right of re-entry or forfeiture under the lease or licence agreement; and

c) Starting or continuing court or insolvency proceedings.

This moratorium does not apply to tenants that are not tenant-occupiers, i.e. they are not operating on the property. It also does not apply to tenant-occupiers that do not meet the criteria for the rental relief, i.e. they are not a SME as defined. The moratorium also does not suspend interest due under lease agreements or license agreement. The moratorium ends when IRAS issues the notice of cash grant to the property owner, or on 31 December 2020 if no such notice is received before then.

What can a landlord do if he is not satisfied that his tenant is eligible for rental relief after reviewing the documents provided by his tenant?

If a landlord and tenant-occupier are unable to reach a compromise, the property owner and/or any intermediary landlord(s) may make an application using the prescribed form here within 10 working days after receiving (a copy of) the notice of cash grant, to have a rental relief assessor ascertain whether the tenant-occupier is eligible for Rental Relief and/or Additional Rental Relief. Please refer to the section Application for Assessment for details.

What if the landlord refuses to grant rental waivers under the rental relief framework? How can tenants ensure that they will receive the rental waivers? Are there any penalties for non-compliance by landlords?

Under the Act, the rent that is payable by eligible tenants to their landlord for the relevant period of rental waiver is statutorily waived once qualifying property owners with eligible tenant-occupiers receive the notice of the cash grant issued by IRAS. This means that as an eligible tenant-occupier you do not need to pay rent for those months.

In the case where tenants have already paid rent for those months for which rent is waived, tenants can apply the rental waivers towards the next most immediate months of rent. If there is insufficient time left in the lease, tenants can obtain a refund from the landlord.

In cases where landlords had earlier provided assistance to their tenants or reached an agreement to provide assistance to their tenants, in the form of monetary payments or reduction of payments due under the lease agreement, or landlords have passed on the benefit of any Property Tax Rebate for Year 2020 in respect of the property, these can be offset from the landlords’ rental waiver obligations.

Why may the sum of the Property Tax Rebate for Year 2020 and the Government cash grant not be equivalent to the rental waiver received by the eligible SME?

The Property Tax Rebate for Year 2020 for non-residential properties and the Government cash grant are based on the Annual Value of the property. This may not be equivalent to the rental waiver to be provided by landlords, which is based on the contractual rent. Tenants will still have to pay for maintenance fee and charges for the provision of services such as cleaning and security. Nevertheless, the landlord is obliged to provide the rental waiver based on the contractual rental as defined, not based on grant by the Government. The Property Tax Rebate and Government cash grant are not intended to cover the full amount of rental waivers exactly.

What can a landlord do if he is unable to afford a rental waiver? What are the eligibility criteria for a landlord to qualify for a halving of the Additional Rental Relief?

The Government recognises that there are landlords who may face genuine financial hardship.Landlords who meet all the following criteria may apply to a rental relief assessor to reduce the amount of Additional Rental Relief they have to provide:

a) The applicant landlord must be an individual or a sole proprietor and is the owner of the prescribed property;

b) The aggregate of the annual value of all investment properties (including the prescribed property) owned (whether solely or jointly with another person and whether directly or through one or more investment holding companies) is not more than S$60,000 as at 13 April 2020; and

c) The rental income derived from the property in question in Year of Assessment 2019 constituted 75% or more of the landlord’s gross income.

If the landlord meets the grounds of financial hardship above, the rental relief assessor may halve the amount of Additional Rental Relief to be borne by the landlord, i.e. one month’s rental waiver for qualifying commercial properties, or half a month’s rental waiver for other non-residential properties (e.g. industrial and office properties). The remaining rent payable will be borne by the tenant.

Property Tax Rebate

*Property Tax Rebate is different from Rental Relief

What is the percentage for property tax rebate?

| Property Type | Component | Tax Rebate |

|---|---|---|

| Hotel | Hotel Rooms | 100% |

| Function Rooms | 100% | |

| Shops, restaurants, gym, tenements such as space for vending machine, base station and tour desk | 100% | |

| Offices that are not used in connection with the operation of the hotel such as serviced offices | 30% | |

| Retail Mall | Shops and restaurants | 100% |

| Offices | 30% | |

| Office Building | Offices | 30% |

| Shops and restaurants | 100% | |

| In-house gym that are used exclusively by the occupants of the office building | 30% |

Are property owners obligated to pass the property tax rebate on to Tenants?

Owners of qualifying properties are required to unconditionally and fully pass on to their tenant(s) the rebate for the property tax account that is attributable to the rented property based on the period it was rented out, by either reducing or offsetting current or future rentals or through a payment to their tenant(s), within the prescribed timeframe.

Failure to properly pass on the rebate, or to keep the records (e.g. information on the amount, manner and time of pass on) until 31 Dec 2023, without reasonable excuse, is an offence. Those guilty of such an offence shall be liable on conviction to a fine not exceeding $5,000.

The property owners are to continue to pass on the rebate to their tenants despite any outstanding objections lodged for the year 2020.

Ministerial Statement – Aug 2020

On 17 August, DPM Heng released a ministerial statement to continue to support jobs and create new ones and provide further support for sectors which are hit the hardest. The continued support will cost $8 billion.

Extension of Jobs Support Scheme ("JSS")

Extension of JSS

The JSS will be extended by up to seven months, covering wages paid up to March 2021. This will provide continued support for businesses and workers amidst the protracted economic downturn.

The table below shows an overview of the support level based on the projected recovery of the various sectors.

Notes:

1. Firms that are not allowed to resume on-site operations will receive Tier 1 JSS support for September 2020 to March 2021 wages or until such time that they are allowed to resume operations on-site, whichever is earlier.

2. Firms in the Built Environment sector will receive Tier 1 JSS support for June to October 2020 wages, and Tier 2 support for November 2020 to March 2021 wages.

Extended JSS Support

Under the extended JSS, sectors are supported at the following tiers for wages paid from September 2020 to March 2021:

- a) Tier 1 sectors (e.g. Aviation, Aerospace, and Tourism) that are currently receiving 75% JSS support, will receive 50% JSS support

- b) Tier 2 sectors (e.g. Food Services, Retail, Marine & Offshore, and Arts and Entertainment) that are currently receiving 50% JSS support, will receive 30% JSS support

- c) Tier 3 sectors that are currently receiving 25% JSS support, will receive 10% JSS support

- This is with the exception of selected Tier 3 sectors (i.e. Financial Services, Information and Communications Technology and Media, Biomedical Sciences, Precision Engineering, Electronics and Online Retail and Supermarkets), which will receive 10% JSS support for wages paid from September to December 2020. JSS support for these sectors will cease after December 2020.

- d) Employers in the Built Environment sector that are currently receiving Tier 1 (75%) JSS support for wages paid June to August 2020, will continue to receive Tier 1 JSS support (at 50%) for wages paid in September and October 2020, and thereafter Tier 2 (30%) support for wages paid from November 2020 to March 2021.

- e) Employers which are not allowed to resume on-site operations during phased re-opening will receive Tier 1 (50%) JSS support for wages paid from September 2020 to March 2021, or until such time when they are allowed to resume operations on-site, whichever is earlier.

For more information, please click here to visit the IRAS JSS website.

List of Sectors In JSS Support Tier – Tier 1

| Sector | Subsector | Qualifying Criteria |

|---|---|---|

| Aviation and Aerospace | Aviation | Consists of: • Airlines • Airport ground handlers • Airport operators |

| Aerospace maintenance, repair, and overhaul (MRO) operators | They must: • Derive more than two-thirds of their revenue from aerospace MRO; and • Have one of the following accreditations or regulatory approvals: (i) Singapore Airworthiness Requirements Part 145 (SAR145) or SAR21 from the Civil Aviation Authority of Singapore (CAAS) (or equivalent from Federal Aviation Administration (FAA)/ European Union Aviation Safety Agency (EASA)); or (ii) National Aerospace and Defense Contractors Accreditation Program (Nadcap); and • Be classified under SSIC 30302. |

|

| Aerospace manufacturing operators | They must: • Derive more than two-thirds of their revenue from aerospace manufacturing; and • Either: be a manufacturing facility of aerospace original equipment manufacturers (OEMs); or have certificates of approved supplier status from aerospace companies; or have the following accreditations or regulatory approvals: (i) SAR145 or SAR21 from CAAS (or equivalent from FAA/EASA); or (ii) Nadcap; and • Be classified under SSIC 30301. |

|

| Major suppliers of parts and services for aerospace MROs and manufacturers | They must: • Carry out one or more of these activities: (a) machining and assembly; (b) tooling; (c) secondary processes; (d) engineering; (e) repair; (f) customised kitting; and (g) inventory management on behalf of aerospace companies and airlines; and • Derive more than two-thirds of their revenue from aerospace companies and airlines; and • Either: have certificates of approved supplier status from aerospace companies; or have the following accreditations or regulatory approvals: (i) SAR145 or SAR21 from CAAS (or equivalent from FAA/EASA); or (ii) Nadcap. |

|

| Airline fleet management services operators | They must: • Derive more than two-thirds of their revenue from aerospace companies, airlines and fleet owners; and • Have the following regulatory approvals: (i) SAR145 or SAR21 from CAAS (or equivalent from FAA/EASA); or (ii) Continuing Airworthiness Management Organization (CAMO) from EASA (or equivalent). |

|

| Operators providing training for pilots and crews | They must: • Be a CAAS-approved Type Rating Training Organisation (or equivalent from FAA/EASA); and • Derive more than two-thirds of their revenue from airlines. |

|

| Tourism, Hospitality, Conventions and Exhibitions | Hospitality, Conventions and Exhibitions Qualifying licensed hotels | They must be a licensed hotel classified under SSIC 551. |

| Qualifying licensed travel agents | They must have more than two-thirds of their revenue from their travel agency business, based on the Annual Business Profile Returns submitted to the Singapore Tourism Board (STB) in 2018. | |

| Qualifying gated tourist attractions | They must: • Have more than 30% visitorship from tourists, and • Be classified under SSICs 91021, 91022, 91029, 91030, 93201, or 93209. |

|

| Cruise | They must be a cruise line or cruise terminal operator. | |

| Meetings, incentives, conferences and exhibitions venue operators (MICE) | They must be purpose-built MICE venue operators. | |

| MICE and tourism event organisers | They must: • Be impacted by the deferment/cancellation/loss of sales of at least one MICE/leisure event with at least 20% foreign attendees (residing outside Singapore) and originally scheduled in Singapore between 1 Feb 2020 to 31 Dec 2020; and • Derive more than two-thirds of their revenue from MICE/leisure events with at least 20% foreign attendees (residing outside Singapore); and • Be classified under SSICs 82301, 82302 or 82303. |

|

| Money changers | They must: • Be licensed by the Monetary Authority of Singapore (MAS) as either “money-changing licensee” or “major payment institution licensee”; and • Derive more than two-thirds of their revenue from money-changing services. |

|

| Regional ferry operators | They must: • Be licensed by the Maritime and Port Authority of Singapore (MPA) as a Regional Ferry Services Operator; and • Be classified under SSIC 50013. |

|

| Central refund agencies | They must be central refund agencies certified by the Inland Revenue Authority of Singapore (IRAS). |

List of Sectors In JSS Support Tier – Tier 1 (Only For June 2020 To October 2020 Wages); Tier 2 Thereafter

| Sector | Subsector | Qualifying Sector |

|---|---|---|

| Built Environment | Built Environment contractors | They must be classified under SSICs 41, 42, or 43. |

| Built Environment consultants | They must: • Be registered with the Public Sector Panel of Consultants; or • Be classified under SSICs 71111, 71113, 71121, or 71125. |

List of Sectors In JSS Support – Tier 2

| Sector | Subsector | Qualifying Criteria |

|---|---|---|

| Food Services | Licensed food shops and food stalls (including hawker stalls) | They must be classified under SSICs 56, or 68104. Licensees registered as individuals will also be included if they make mandatory CPF contributions for their employees. |

| Retail | Qualifying retail outlets | They must: • Hold a valid Film Exhibition licence from the Infocomm Media Development Authority (IMDA); and • Be classified under SSIC 5914. |

| Arts and Entertainment | Cinema operators | They must: • Hold a valid Film Exhibition licence from the Infocomm Media Development Authority (IMDA); and • Be classified under SSIC 5914. |

| Film distributors | They must: • Have transacted with IMDA to classify films for exhibition in cinemas between 1 Apr 2019 to 31 Mar 2020; and • Be classified under SSICs 59131 or 59139. |

|

| Arts and Culture organisations | They must: • Meet at least one of the conditions of being a: (i) participant in a project, activity, programme or festival supported by the National Arts Council (NAC) or National Heritage Board (NHB) between 1 April 2018 to 31 March 2020; (ii) Museum Roundtable member before 31 March 2020; or (iii) accredited Arts Education Programme (AEP) provider listed in the 2019-2021 NAC-AEP Directory; and • Be classified under SSICs 85420, 90001, 90002, 90003, 90004, 90009, 91021, 91022, or 91029. |

|

| Land Transport | Rail operators | They must: • Hold a Land Transport Authority (LTA) New Rail Financing Framework licence; and • Not receive service payments from the Government for the operation of rail services; and • Derive more than two-thirds of their revenue from rail-related activities. |

| Point-to-Point (P2P) transport operators | They must hold an LTA taxi service operator licence; or an LTA third-party taxi booking service operator licence. | |

| Private bus and limousine operators | They must: • Have “P” plate buses or sedans/multi-purpose vehicles (MPVs) registered as Z10, Z11, R10, R11 vehicles; and • Be classified under SSICs 49212, 49219, 77101, or 52299. |

|

| Marine and Offshore | Marine and Offshore | They must: • Derive more than two-thirds of their revenue from the following activities: (i) manufacture and repair of oil rigs; (ii) building of ships, tankers and other ocean-going vessels (including conversion of ships into off-shore structures); (iii) repair of ships, tankers and other ocean-going vessels; (iv) manufacture and repair of marine engine and ship parts; and/or (v) manufacture and repair of oilfield and gas field machinery and equipment components (e.g. derricks, tool joints, process modules and packages); and • Be classified under SSICs 30110, 28112, 28241, or 28242. |

| Sector | Subsector | Qualifying Criteria |

|---|---|---|

| Biomedical Sciences | Biomedical Sciences | They must be classified under SSICs 21011, 21012, 21013, 2102, 2103, 266, 325, 46461, 46592, 72101, 72107, or 72109. |

| Precision Engineering | Precision Engineering | They must be classified under SSICs 22191, 22192, 22193, 22199, 22211, 22214, 22215, 22216, 22218, 22219, 2222, 25113, 2513, 2591, 2592, 2593, 2594, 25951, 25959, 25993, 25995, 25997, 25998, 25999, 26127, 2651, 2652, 2670, 271, 273, 28111, 2812, 2814, 2815, 2816, 2818, 2819, 2822, 28243, 28249, 2825, 2826, 2827, 2829, or 283. Electronics Electronics They must be classified under SSI |

| Electronics | Electronics | They must be classified under SSICs 2611, 26121, 26122, 26123, 26124, 26125, 26126, 26129, 262, 263, 264, or 26801. |

| Financial Services | Financial Services | They must: • Be classified under SSICs 641, 643, 649, 65, and 66; or • Be MAS-regulated firms classified under SSIC 642. |

| Information and Communications Technology and Media | Information and Communications Technology | They must be classified under SSICs 4651, 46521, 46523, 46591, 58202, 61, 62011, 62013, 62014, 62019, 6202, 6209, 631, 63909, 72105, 74111, 77341, 78101, 822, or 9511. |

| Media | They must be classified under SSICs 46444, 581, 58201, 60, 62012, 63901, or 9101. | |

| Postal and Courier | They must be classified under SSIC 53. | |

| Retail | Supermarkets and Convenience Stores | They must be classified under SSICs 4711, or 47192. |

| Online Retail | They must be classified under SSIC 4791. | |

| Tier 3A: Others (JSS support till March 2021) | ||

| Others | All other employers | N/A |

For more information, please click here to visit the IRAS JSS website.

Extension of Workfare Special Payment ("WSP")

As part of the Care and Support Package announced at Budget 2020, all Singaporean employees and Self-Employed Persons (SEPs) who received Workfare Income Supplement (WIS) payment for Work Year (WY) 2019 are receiving a $3,000 Workfare Special Payment (WSP) in 2020. The first payment of $1,500 was made to eligible Singaporeans in July 2020. They will receive their next and final tranche of WSP ($1,500) in October 2020.

The WSP has been extended to include lower-wage workers aged 35 and above in 2020 who received WIS payment for WY2020, and who have not already qualified for WSP previously (see Table 1). A one-off payment of $3,000 will be given to eligible individuals from October 2020 onwards.

Click here to find out more on the Care and Support Package can be found at the Care and Support Package.

Jobs Growth Incentive ("JGI")

There are bright spots amidst the severe economic situation especially in healthcare, F&B, manufacturing, biomedical sciences, financial services, and ICT sectors where they are constantly needing more workers. To support hiring in growing sectors, the Jobs Growth Incentive, or JGI will be launched. The JGI supports the Government’s efforts to create new jobs for workers, with a special focus on mature workers. $1 billion have been set aside to support firms to increase their headcount of local workers over the next six months.

For each new local hire, Government will provide wage subsidy for 12 months:

• Up to 25% for those below 40 years old, subject to cap

• Up to 50% for those aged 40 and above, subject to cap

More details about this programme will be released later this month.

COVID-19 Support Grant

The Covid-19 Support Grant (CSG) was introduced in May to complement the ComCare scheme in these extraordinary times. More than 60,000 residents have benefited, with more than $90 million disbursed so far.

• The application period has been extended up to December 2020

• Open to both existing CSG recipients and new applicants from 1 October 2020

• Unemployed applicants must demonstrate job search or training efforts to qualify

The Ministry of Social and Family Development will share more details in early September.

Preserving Core Capabilities

Further support for hardest-hit sectors such as aerospace, aviation, and tourism to retain core capabilities.

• $187 million to extend support measures in the Enhanced Aviation Support Package up to March 2021. This package includes cost relief to our airlines, ground handlers, cargo agents and airport tenants so as to support local carriers to regain Singapore’s air connectivity to the world.

• Temporary redeployment programme scaled up for workers in the aviation sector

• $320 million to boost domestic tourism through tourism credits for Singaporeans (SingapoRediscovers Vouchers)

Startup SG Founder programme

To continue to spur innovation and entrepreneurship, up to $150 million has been set aside. The government will raise the startup capital grant and continue to provide mentorship.

The Ministry of Trade and Industry will provide more details about the StartupSG Fouder Programme later this week.

China’s Income Tax Policy in Relation to Overseas Income

On 17 January 2020, China’s Ministry of Finance and State Taxation Administration jointly issued the “Announcement on Individual Income Tax Policy in relation to Overseas Income” (Ministry of Finance and State Taxation Administration Announcement 3 of 2020). This announcement applies from the 2019 tax year. This means that income earned overseas by China tax residents will be taxed.

Announcement 3 sets out the relevant policies regarding this new income tax policy. The key contents include:

- Classification of overseas income

- Calculation of taxable income

- Foreign tax credit (“FTC”)

Residence rules

An individual is domiciled in China if:

(a) They habitually reside in China by reason of permanent registered address, family ties, or economic interests; or

(b) holds a Chinese passport or a hukou (household registration).

Classification of Overseas Income

The following categories of income are considered as overseas income:

| Income categories | Basis of income sourcing |

|---|---|

| (1) Income from provision of labour services outside China (including employment income and independent personal service income) | The overseas location where the labour or employment activities are carried out. |

| (2) Authors’ remuneration paid and borne by enterprises and other organisations outside China; | The overseas location of the enterprise or organisation which pays and bears the remuneration. |

| (3) Royalties received from the grant of concessions outside China; | The overseas location where the concessions are utilised. |

| (4) Income from business operations and productions outside China; | The overseas location where business operation or production is carried out. |

| (5) Interest and dividend income obtained from enterprises, other organisations and non-resident individuals outside China; | The overseas location where the interest and/or dividend paying parties are based. |

| (6) Income from lease of overseas properties; | The overseas location where the leased property is used. |

| (7) Capital gains from the transfer of real estate, transfer of equity stocks, stock options, or other financial assets (hereinafter referred to as financial assets) of overseas enterprises or other organisations, or from the transfer of other assets outside China; | Real estate: the overseas location where the asset is located; Financial assets: the overseas location where the invested enterprise or other organisation is based. It is worth noting that if more than 50% of the fair value of the assets of the invested enterprise or other organisation comes directly or indirectly from real estate located in China at any time during the three years (36 consecutive months) prior to the transfer, the gains from the transfer of the assets would be deemed as China sourced. |

| (8) Incidental income obtained from enterprises, other organisations and non-resident individuals outside China; | The overseas location where the incidental income paying parties are based. |

| (9) Separate rules may apply if otherwise determined by the Ministry of Finance or the State Taxation Administration. | N/A |

Personal Income Tax Rate

The following table shows the latest Income Tax Rate for residents in China.

| Annual taxable income (CNY) | Tax rate (%) | Quick deduction (CNY) |

|---|---|---|

| 0 to 36,000 | 3 | 0 |

| Over 36,000 to 144,000 | 10 | 2,520 |

| Over 144,000 to 300,000 | 20 | 16,920 |

| Over 300,000 to 420,000 | 25 | 31,920 |

| Over 420,000 to 660,000 | 30 | 52,920 |

| Over 660,000 to 960,000 | 35 | 85,920 |

| Over 960,000 | 45 | 181,920 |

How to calculate Taxable Income?

Domestic and foreign income subject to consolidated tax calculation

Comprehensive income

Annual comprehensive income = comprehensive income within China + comprehensive income from overseas

Income from business operations

Annual operating income = income from domestic operations + income from overseas operations

Losses from business operations in a particular overseas jurisdiction cannot be offset against income from operations in China or other overseas locations. However, the losses may be used to offset business operating income at the same location in future tax years, based on the relevant tax law in China.

Domestic and foreign income subject to separate tax calculation

Income derived from interest, dividends, property lease, property transfer, and incidental income cannot be consolidated with China-sourced income and shall be subject to tax calculation separately.

Foreign Tax credit ("FTC")

Announcement 3 makes it clear that where resident taxpayers receive overseas income during a tax year, FTC will be granted where foreign income tax has been paid in the overseas location in accordance with the tax law in that jurisdiction, subject to limits. The formula is as follows:

Tax / refund due for the tax year = total tax liability for the tax year – overseas tax liability allowable as credit (not exceeding the tax credit limit)

The amount of overseas tax exceeding the tax credit limit can be utilised in the following five tax years.

Overseas income not allowed for FTC

The following are the circumstances that are not allowed and shall be excluded from the FTC claim:

- Overseas tax paid or collected by mistake;

- Tax which should not be levied in the overseas jurisdiction under the Double Tax Treaty between China and the foreign country (or under the Double Tax Arrangement between Mainland China and Hong Kong and Macao);

- Late payment interest and/or penalties imposed by overseas tax authorities for underpayment or late payment of overseas income tax;

- Overseas income tax which is due for refund or compensation from the overseas tax authorities;

- Overseas income which is tax-exempt under the China IIT Law and Implementation Rules.

Singapore’s Tax Treaty with China

As there is an agreement between The Government of The Republic of Singapore and The Government of The People’s Republic of China, China residents receiving an income from Singapore or vice-versa, will be eligible for double tax relief if conditions are met. However, this is not an exemption of tax, but rather a reduction of tax.

According to Article 22 of the treaty, elimination of double taxation in China shall be eliminated as follows:

(a) Where a resident of China derives income from Singapore the amount of tax on that income payable in Singapore in accordance with the provisions of this Agreement, may be credited against the Chinese tax imposed on that resident. The amount of the credit, however, shall not exceed the amount of the Chinese tax on that income computed in accordance with the taxation laws and regulations of China.

(b) Where the income derived from Singapore is a dividend paid by a company which is a resident of Singapore to a company which is a resident of China and which owns not less than 10 per cent of the shares of the company paying the dividend, the credit shall take into account the tax paid to Singapore by the company paying the dividend in respect of its income.

In Singapore, double taxation shall be avoided as follows:

(a) Where a resident of Singapore derives income from China which, in accordance with the provisions of this Agreement, may be taxed in China, Singapore shall, subject to its laws regarding the allowance as a credit against Singapore tax of tax payable in any country other than Singapore, allow the Chinese tax paid, whether directly or by deduction, as a credit against the Singapore tax payable on the income of that resident.

(b) Where such income is a dividend paid by a company which is a resident of China to a resident of Singapore which is a company owning directly or indirectly not less than 10 per cent of the share capital of the first-mentioned company, the credit shall take into account the Chinese tax paid by that company on the portion of its profits out of which the dividend is paid.

Note:

Singapore employment income is not taxed in China according to the provisions of Articles 16, 18 and 19 of the treaty, salaries, wages and other similar remuneration derived by a resident of a Singapore State in respect of an employment shall be taxable only in Singapore unless the employment is exercised in the China. If the employment is so exercised, such remuneration as is derived therefrom may be taxed in China.

When it comes to profits earned from interest, royalties and dividend payments, special reduced rates apply, as follows:

Dividends

Dividends paid by a company which is a resident of China to a resident of Singapore may be taxed in Singapore.

However, such dividends may also be taxed in China of which the company paying the dividends is a resident and according to the laws of that State, but if the beneficial owner of the dividends is a resident of Singapore, the tax so charged shall not exceed:

(a) 5 per cent of the gross amount of the dividends if the beneficial owner is a company (other than a partnership) which holds directly at least 25 per cent of the capital in the enterprise paying the dividends;

(b) in all other cases, dividend payments are taxed at a rate of 10%.

Interest

Income arising from interest issued by a bank or financial institution which is a resident of China to a resident of Singapore, may be taxed in Singapore.

However, such interest may also be taxed in China of which the bank or financial institution paying the interest is a resident and according to the laws of that State, but if the beneficial owner of the interest is a resident of Singapore, the tax so charged shall not exceed:

(a) 7 per cent of the gross amount of the interest if it is received by any bank or financial institution

(b) 10 per cent of the gross amount of the interest in all other cases.

Royalties

Royalties in this treaty means payments of any kind received as consideration for the use of, or the right to use, any copyright of literacy, artistic or scientific work including cinematograph films, or films or tapes for radio or television broadcasting, any computer software, patent, trade mark, design or model, plan, secret formula or process, or for the use of, or the right to use, industrial, commercial or scientific equipment or for information concerning industrial, commercial or scientific experience.

These royalties derived from China and paid to a resident of Singapore, may be taxed in Singapore, and vice-versa.

However, if the beneficial owner of the royalties is a resident of Singapore, the tax charged shall not exceed 10 per cent of the gross amount of the royalties.

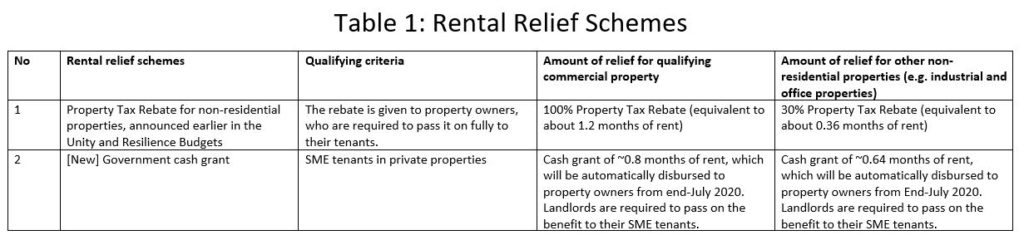

Rental Relief For SME Tenants In Private Non-Residential Properties

For SME tenants (i.e. with not more than $100 million in annual turnover) with qualifying leases or licences commencing before 25 March 2020, the Government will provide a new cash grant to offset their rental costs as stated in Table 1.

SME property owners who run a trade or business on their own property will also be eligible for the new cash grant. Vacant property and land under development will not be eligible.

Implementation of the New Government Cash Grant

The new government cash grant will be disbursed automatically by IRAS to the qualifying property owners.

The amount of grant will be calculated based on the Annual Values of properties for 2020, as determined by IRAS at 13 April 2020.

For property owners whose properties are only partially let out, or whose properties are let out to both SME and non-SME tenants under a single property tax account, they will not automatically receive the government cash grant.

In such instances, the property owner should submit an application to IRAS, and provide supporting documents, including proof of SME tenants within its property. IRAS will pro-rate the government cash grant accordingly.