Corporate Income Tax (CIT) Rebate – YA 2026

Purpose: Provide operating cost relief to all active companies to support cash flow and competitiveness.

Details

Rebate Rate: 40 % of corporate tax payable for Year of Assessment (YA) 2026.

Minimum benefit: S$1,500 (if company employed at least one local worker in 2025).

Cap: S$30,000 total benefit (rebate + cash grant)

Enterprise Innovation Scheme (EIS)

Purpose: Encourage innovation, capability building and tech adoption (including AI) through enhanced tax deductions.

Under EIS, companies can claim up to 400% tax deductions or allowances on qualifying expenditures. Eligible businesses may also opt to convert part of the qualifying expenditure into a 20% non-taxable cash payout, subject to conditions.

Qualifying Activities (existing base)

Qualifying R&D conducted in Singapore.

Registration of Intellectual Property (IP) rights.

Acquisition/licensing of IP rights.

Training courses eligible for SkillsFuture funding aligned to the national Skills Framework.

Innovation projects with approved partner institutions (e.g., polytechnics, ITE).

New AI-related Activity

From YA 2027 to YA 2028, qualifying AI-related expenditure will be added to the list of activities eligible for 400% deduction.

Important Clarification:

AI-related expenditure is not eligible for the cash conversion option (see below).

The enhanced deduction applies only to qualifying AI adoption and implementation costs as defined by IRAS.

Typical AI-related spend that may qualify:

- AI platform subscriptions used for business transformation

- Implementation costs for AI systems integrated into workflows

- Fees for AI development services

(The final scope of qualifying AI expenditure will be published by IRAS.)

Market Readiness Assistance (MRA) Grant

Purpose: Help companies defray costs of entering and expanding in overseas markets (overseas promotion, business development, set-up).

Pre-Budget (Prior Structure)

SMEs could get 50 % co-funding, capped at S$100,000 per company per new market.

Eligible activities included trade fair participation, overseas partner searches, overseas staff deployment, and advisory/legal services.

Budget 2026 Enhancements

Support levels:

SMEs: Up to 70 % of eligible costs (from 1 Apr 2026 until 31 Mar 2029).

Non-SMEs: Up to 50 % of eligible costs.

Enhanced cap S$100,000 per company per market continues.

The prior requirement of selling <S$100,000 in a target market to qualify is phased out later in 2026.

Where To Apply

Applications via Business Grants Portal Website: https://www.enterprisesg.gov.sg/financial-support/market-readiness-assistance-grant

Check EnterpriseSG for eligibility details and documentation.

Double Tax Deduction for Internationalisation (DTDi)

Purpose: Support companies expanding overseas by allowing enhanced tax deductions on internationalisation expenses.

Qualifying Activities (Expanded)

Businesses can automatically claim a 200 % tax deduction on qualifying expenses up to S$400,000 per YA (raised from S$150,000). Qualifying activities (without prior approval) now include:

Overseas market development and investment study trips.

Market feasibility and surveys.

Master licensing and franchising costs.

Overseas business development (e.g., trade visits).

Production of corporate brochures for overseas distribution.

Note: Expenses beyond S$400,000 or specific campaigns (trade offices, e-commerce campaigns) still require approval by EnterpriseSG or Singapore Tourism Board.

Where To Apply/Claim

Claim via the company’s tax return (Form C) with supporting documentation.

Prior approval for large or special categories through EnterpriseSG/STB as needed.

Enterprise Financing Scheme (EFS)

Purpose: Provide financing support and credit for business expansion (trade, working capital and asset financing).

Budget 2026 Enhancements

Higher loan quantum options for trade and fixed asset loans.

Overall exposure cap raised to up to S$50 million per borrower (group cap).

This allows larger firms or groups to access higher financing limits under the scheme.

Where To Apply

Via Enterprise Singapore’s EFS portal (accessible through the Business Grants Portal or EnterpriseSG site).

Applications involve business financials, loan purpose, and risk assessment.

Startup SG Equity Scheme

Purpose: Government co-invests with independent private investors into Singapore-based startups to catalyse funding and growth.

Budget 2026 Investment

S$1 billion top-up to support both early-stage and growth-stage companies.

Where To Apply / Eligibility

Administered by Enterprise Singapore / SEEDS Capital / EDBI.

Typical eligibility (for early-stage startups):

Singapore-incorporated private limited company.

Innovative product/service with IP or strong technical foundation.

Scalable business with global market potential.

A ready, independent third-party investor (e.g., VC) for co-investment engagement.

How To Apply

Contact EnterpriseSG, SEEDS Capital or EDBI directly (find contacts via EnterpriseSG soft-landing pages).

Submit company profile, business plan, financials and investor term sheet.

Champions of AI Programme

Purpose: Help companies adopt and scale enterprise-wide AI transformation.

What It Is

A new initiative to provide tailored support to companies undertaking comprehensive AI adoption — beyond point solutions.

May include transformation planning, capability building, workforce training and advisory support.

Where To Find Details

Exact scheme details and application modalities are likely to be announced by Enterprise Singapore or government agencies in 1H 2026. (Watch EnterpriseSG and MOF announcements.)

Add Your Heading Text Here

Senior Employment Credit (SEC)

Purpose: Provide wage offsets to help employers hire and retain senior Singaporean workers.

Details (Post-Budget 2026)

Extended until 31 Dec 2027.

Employers receive wage offsets for Singaporean workers aged 60+ earning under S$4,000 per month.

Offset rates vary by age band, up to 7 % of wages (for older age tiers).

How It Works

Payouts are automatic (through IRAS) if eligibility conditions are met — no separate application required.

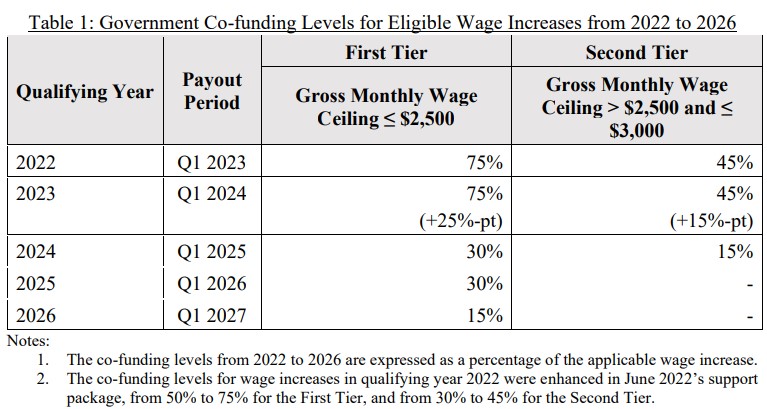

Progressive Wage Credit Scheme (PWCS)

Purpose: Help employers adjust to mandatory wage increases and voluntarily raise wages of lower-wage workers.

Key Features

Co-funding support for wage increases of eligible resident employees continues through 2026.

2025: 40 % co-funding; 2026: 20 % co-funding (on qualifying wage increases).

Employers do not need to apply — payouts are computed and disbursed based on CPF contribution data.