黄金山 會計公司

A supply spans the change of GST rate where one or two of the following events takes place wholly or partially on or after 1 Jan 2023:

If you issue an invoice for your supply on or after 1 Jan 2023 but you receive full payment before 1 Jan 2023, the supply is subject to 7% GST.

If you issue an invoice for your supply on or after 1 Jan 2023 but you have delivered all the goods or performed all the services before 1 Jan 2023, the entire value of the supply is subject to 7% GST.

If you have received full payment before 1 Jan 2023, or if you have delivered all the goods or performed all the services before 1 Jan 2023, the entire value of the supply is subject to 7% GST.

If you do not receive full payment before 1 Jan 2023 and you have delivered or performed a part or all of the goods or services before 1 Jan 2023, you can elect to charge 7% GST on the higher of:

(a) The payment received is before 1 Jan 2023; or

(b) The value of goods delivered or services performed is before 1 Jan 2023.

The remaining value of the supply will be subjected to 8% GST.

On 22 Dec 2022, you issue a tax invoice for your supply of services (value of $1,000) and you receive the full payment on 5 Jan 2023. You perform part of the services (value of $200) before 1 Jan 2023 and the remaining part of the services (value of $800) after 1 Jan 2023.

You must charge and account for GST at 7% ($70) for the tax invoice issued to your customer on 22 Dec 2022. As you do not receive any payment and only perform part of the services before 1 Jan 2023, under the transitional rules, you are required to issue the following to your customer by 15 Jan 2023, for that part of the services performed after 1 Jan 2023:

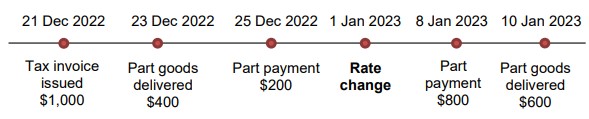

On 21 Dec 2022, you issue a tax invoice for your supply of services (value of $1,000). Before 1 Jan 2023, you delivered part of the goods (value of $400) and received a payment of $200. After 1 Jan 2023, you receive the remaining payment of $800 and perform delivered the other part of the goods (value of $600).

Under the transitional rules, you are required to issue the following by 15 Jan 2023, for that part of the goods delivered after 1 Jan 2023:

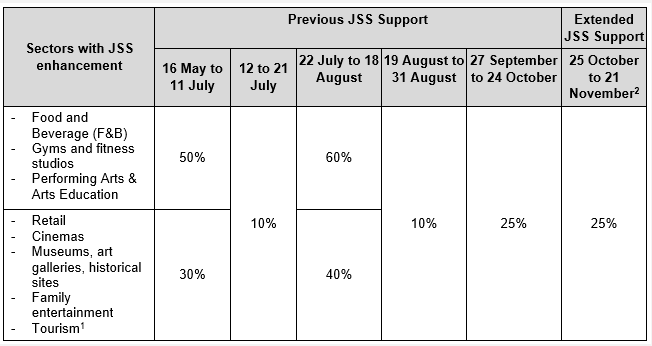

From 25 October to 21 November 2021 onwards, the Government will provide enhanced JSS support for the following sectors:

The enhanced payout corresponding to wages paid for Aug to Oct 2021 will be disbursed in December 2021. Employers who put local employees on mandatory no-pay leave (NPL) or retrench them will not be entitled to the enhanced JSS payouts for those employees.

If your company has an existing GIRO arrangement with IRAS or is registered for PayNow Corporate as at 24 Sep 2021, you will receive a payout titled “Jobs Support Scheme” (GIRO) or “GOVT” (PayNow Corporate) in your bank account from 30 Sep 2021. Other employers will receive their cheques from 15 Oct 2021 mailed to their registered business address.

As part of the checks for JSS eligibility, a small number of employers will receive letters from IRAS asking them to conduct a self-review of their CPF contributions and to provide declarations or documents to substantiate their eligibility for JSS payouts. Their Sep 2021 payout will be withheld pending the self-review and verifications by IRAS. The payout will only be disbursed after the completion of the review. If your company has been selected for self-review, please refer to Self-review for Eligibility of JSS and JGI for more information.

From 25 October to 21 November 2021 onwards, the Government will provide enhanced JSS support for the following sectors:

The enhanced payout corresponding to wages paid for Aug to Oct 2021 will be disbursed in December 2021. Employers who put local employees on mandatory no-pay leave (NPL) or retrench them will not be entitled to the enhanced JSS payouts for those employees.

If your company has an existing GIRO arrangement with IRAS or is registered for PayNow Corporate as at 24 Sep 2021, you will receive a payout titled “Jobs Support Scheme” (GIRO) or “GOVT” (PayNow Corporate) in your bank account from 30 Sep 2021. Other employers will receive their cheques from 15 Oct 2021 mailed to their registered business address.

As part of the checks for JSS eligibility, a small number of employers will receive letters from IRAS asking them to conduct a self-review of their CPF contributions and to provide declarations or documents to substantiate their eligibility for JSS payouts. Their Sep 2021 payout will be withheld pending the self-review and verifications by IRAS. The payout will only be disbursed after the completion of the review. If your company has been selected for self-review, please refer to Self-review for Eligibility of JSS and JGI for more information.

Construction firms here will soon be able to seek relief for higher foreign manpower costs from their contract partners if their workers’ salaries have been affected as a result of Covid-19-related measures.

This will be done through an amendment to the Covid-19 (Temporary Measures) Act Bill that was introduced in Parliament on Monday (May 10).

Under the amended law, affected contractors, including sub-contractors, may apply to the authorities for an assessor to adjust the contract sum to take into account an increase in foreign manpower salary incurred between Oct 1 last year and Sept 30 this year due to reasons relating to Covid-19.

Part 10A of he Covid-19(Temporary Measures) Act has come into operation on 6 August 2021. Part 10A provides a framework for parties to construction contracts to apply for relief from their contractual counterparties if they are affected by an increase in cost of work permit holders due to the Covid-19 events such as border control quotas set by Government limiting the inflow of foreign workers.

COTMA Part 10A (which commenced on 06 August 2021) allows contractors in eligible contracts to apply to an independent Assessor. The Assessor has the power to adjust the contract sum of eligible construction contracts taken into consideration of the increase in foreign manpower salary cost incurred anytime during the period from 01 October 2020 to 30 September 2021 (both dates inclusive).

Criteria:

Contractors must show proof of reasonable attempts to negotiate with their clients before they can apply to an Assessor.

Party A must first apply to the Registrar for the Appointment of an Assessor.

Response from Registrar

If the Registrar is satisfied with the application, he/she will end to Party A the following:

Notifying respondents

Party A must serve a copy of the application and the Registrar Response to the following parties within two working days after the date Party A receives the response

Party A must then, within two working days after the service of the copy of the application and the Registrar Response to the above parties, submit to the Registrar a declaration in Form C of such service.

Application fee

Once the relevant parties have been notified and the Form C declaration has been submitted, the Registrar will inform Party A of the application fee and the payment procedure. The application fee is based on the increase in the amount of foreign manpower salary costs incurred (the amount of foreign manpower salary costs incurred because of a COVID-19 event minus the amount of foreign manpower salary costs that would have been incurred in a circumstance without COVID-19

Refer to this table to ascertain the fee payable for an application.

Once the prescribed application fee is paid the Registrar will send a notice of the appointment of an Assessor to Party A and inform the date and place for the hearing if applicable.

Response from respondents

If Party B wishes to contest an application, they must submit to the Registrar a response to the application via Form D no later than five working days after being serve the copy of the application and the Registrar Response by Party A.

The response must also be served on:

Assessor’s determination

The Assessor will them determine whether:

Other Forms (only to be submitted when applicable):

The enhanced payout corresponding to wages paid for Aug to Oct 2021 will be disbursed in December 2021, while the enhanced payout corresponding to wages paid in Aug 2021 will be disbursed in December 2021. As JSS payouts are intended to offset and protect local employees’ wages, employers who put local employees on mandatory no-pay leave (NPL) or retrench them will not be entitled to the enhanced JSS payouts for those employees.

| Sector | Eligibility Criteria | Current JSS Support (1 Apr 2021 – 15 May 2021) | Enhanced JSS Support (16 May 2021 – 13 Jun 2021*) |

|---|---|---|---|

| Food and Beverage | Entities must be classified under SSICs 56, or 68104. Licensees registered as individuals will also be included if they make mandatory CPF contributions for their employees. | 10% | 50% |

| Performing Arts & Arts Education | Entities must: • Meet at least one of the conditions of being a: (i) participant in a project, activity, programme or festival supported by the National Arts Council (NAC) or National Heritage Board (NHB) between 1 April 2018 to 31 March 2021; or (ii) Museum Roundtable member before 31 March 2021; or (iii) accredited Arts Education Programme (AEP) provider listed in the 2019-2022 NAC-AEP Directory; or (iv) has more than two-thirds of its business in arts/heritage related activities (as defined by one of the 6 qualifying SSICs in criterion 2); and • Be classified under SSICs 85420, 90001, 90002, 90003, 90004 or 90009. | 10% | 50% |

| Sports | Gyms, fitness studios and other sports facilities that must: • Be classified under SSIC 93111, 93119, 93120 or 85410; and • Operate sports- and/or fitness-related programmes that are (i) conducted indoors without masks on prior to P2(HA); or (ii) for those 18 years and under prior to P2(HA). | 0% | 50% |

| Retail | Qualifying retail outlets must: • Have physical storefronts; and • Be classified under SSICs 47191, 47199, 474, 475, 476, 4771, 47721, 4773, 4774, 47752, 47759, 47761, 47769, 4777, 47802, or 4799. | 10% | 30% |

| Cinema operators | Entities must: • Hold a valid Film Exhibition licence from the Infocomm Media Development Authority (IMDA); and • Be classified under SSIC 5914. | 10% | 30% |

| Museums, art galleries and historical sites | Entities must: • Meet at least one of the conditions of being a: (i) participant in a project, activity, programme or festival supported by the National Arts Council (NAC) or National Heritage Board (NHB) between 1 April 2018 to 31 March 2021; (ii) Museum Roundtable member before 31 March 2021; or (iii) accredited Arts Education Programme (AEP) provider listed in the 2019-2022 NAC-AEP Directory; or (iv) has more than two-thirds of its business in arts/heritage related activities (as defined by one of the 6 qualifying SSICs in criterion 2); and • Be classified under SSICs 91021, 91022, 91029 | 10% | 30% |

| Indoor playgrounds and other family entertainment centres | Entities must: • Be classified under SSICs 93201 or 93209; and • Operate family entertainment centres or family attractions-related businesses. | 0% | 30% |

| Indoor playgrounds and other family entertainment centres | Entities must: • Be classified under SSICs 93201 or 93209; and • Operate family entertainment centres or family attractions-related businesses. | 0% | 30% |

| Affected Personal Care Services | Entities must: • Be classified under SSIC 96022 or 96029; • Have physical storefronts; and • Operate personal care services that require masks to be removed (e.g. facial and spa) | 0% | 30% |

Ministry of Sustainability and the Environment on 22 May 2021, we will subsidise 100% of fees for table-cleaning and centralised dishwashing services for around 6,000 cooked food stallholders in hawker centres managed by the National Environment Agency (NEA) or NEA-appointed operators during the no dine-in period.

One-off support for lower- to middle-income employees and self-employed persons who are financially impacted as a result of the tightened measures. Individuals who experience at least one month of involuntary NPL or income loss of at least 50% for at least one month, during the period between 16 May 2021 and 30 June 2021 may apply for CRG-T.

Who can apply?

Note: Businesses of similar nature but have different SSIC codes i.e. 85410, 93119, 93120 can apply for Sport Singapore’s assessment.

A Singapore Family Office usually refers to an entity which manages assets for or on behalf of only one family and is wholly owned or controlled by members of the same family. The term ‘family’ in this context refers to individuals who are lineal descendants from a single ancestor, as well as the spouses, ex-spouses, adopted children and step children of these individuals.

SFOs are exempted from engaging in fund management and financial advisory activities from licensing requirements. Under the statutory exemptions, an SFO may be exempted from licensing requirements if it was structured as either (a) a corporation which manages funds for its related corporations, or (b) a corporation that provides financial advisory services to its related corporations.

MAS may consider the following to be of a SFO arrangement:

The business would need to have an interview with the MAS, which we will help to coordinate and prepare the client for.

After incorporation of the Single Family Office, various holding companies would be incorporated under the family office structure. There are some conditions that must be met if the corporation wants to qualify for the Enhanced Tier Fund Tax Exemption Scheme (also known as Section 13X).

For example, the office would need to hire at least three investment professionals, invest at least S$50 million into the fund entity and have local business spending of at least $200,000 a year.

The business would have to go through an interview with the MAS, which we will help to coordinate and prepare the client for as well as to see an investment strategy before granting approval for the business to qualify for Section 13X tax exemption.

The 13X exemption allows specified income derived from certain designated investments to be exempted from tax. The designated investments include a wide range of assets such as stocks, shares, securities and derivatives.

Family offices in Singapore could apply for a tax incentive under the Financial Sector Incentive-Fund Management Scheme (FSI-FM) which incentivises fund management and the provision of investment advisory services in Singapore.

Under this scheme, fee income derived by a Singapore fund manager from managing or advising a qualifying fund is taxed at a rate of 10% instead of the usual corporate tax rate of 17%.

To qualify for the scheme, a fund manager must hold a Capital Markets Services (CMS) licence, employ at least 3 experiences investment professionals earning at least S$3,500 per month and have a minimum AUM of S$250 million. This is very relevant for large family offices, where the scale of operations and the income derived from managing or advising qualifying funds could be substantial.

The company must first decide where the family office will be located in order to set up the family office. Other administrative tasks include establishing family governance guidelines and come up with a Family Constitution, opening of bank accounts, implementing IT systems for portfolio aggregation and so on.

On 17 August 2020, Deputy Prime Minister Heng Swee Keat announced during his Ministerial Speech that S$150 million has been set aside for the enhancement of the Startup SG Founder scheme.

First-time entrepreneurs will be able to access a higher start-up capital grant of S$50,000, up from $30,000, to help them launch their business ideas. In addition to the increase in the start-up grant, a three-month venture building programme has also been introduced to help start-ups get their innovative ideas off the ground.

The reason for the enhancement of the scheme is to spur new development and new growth opportunities. Besides new innovations and solving real world problems, start-ups also help to create more and new types of job opportunities for Singaporeans. By enhancing the Startup SG Founder programme, the government hopes to enable more aspiring entrepreneurs to start new ventures and accelerate the formation of innovative startups in Singapore.

Under the “Train” track scheme, Enterprise Singapore has appointed Venture Builder and Accredited Mentor Partners (‘VB-AMPs’) with strong track records of venture building to provide 3-month Venture Building (VB) programmes to Singaporeans. The programme will provide support for sourcing innovation, commercialising these ideas into scalable businesses, getting product/solution validation from customers and finding capital.

To be eligible for this track, applicants must fulfil the following criteria:

i. Singaporean Citizen or Permanent Resident;

ii. Commit to 100% attendance for the Venture Building Programme;

iii. Commit to running a startup full time after the programme.

They will also need to pass the VB-AMPs’ screening criteria, which is not limited to:

aptitude, expertise, background and related experience.

The table below summarises the eligibilities of different categories of individuals. The

list below is non-exhaustive, and subject to changes by ESG. Categories of individuals

not listed below will be assessed for eligibility on a case-by-case basis by ESG.

| Category | Eligibility for the VB Programme | Eligibility for Stipends | |

|---|---|---|---|

| Applicants who are full time employed, part-time employed, self-employed or freelancing | |||

| 1 | Applicants who are currently in part-time or full-time employment | No, unless applicants are willing to tender the resignations before enrolling into the programme. | If programme-eligible applicants are still serving notice during the programme, pro-rated stipends will be provided after the notice period ends |

| 2 | Freelancers | Yes, provided applicant can be full time committed to the Venture Building Programme | Yes |

| 3 | Self employed | i. If the business is registered as a sole proprietor, the treatment for freelancers (case #2) will apply. ii. For all other business entities, the treatment will follow that of case #5. |

|

| Former / current startup founders | |||

| 4 | Applicants who have previously incorporated a business entity on ACRA (ie. Pte Ltd / LLC / any other business entities), which was nonrevenue generating and is no longer active | Yes | Yes |

| 5 | Applicants with a business entity that is active and live on ACRA, registered as Pte Ltd / LLC / any other business entities, excluding sole proprietorship | No. If your business entity is a startup, you may wish to apply for the Startup SG Founder grant, provided you meet the eligibility criteria. | No |

| 6 | Applicants who have been awarded the Startup SG Founder grant | No | No |

| Students | |||

| 7 | Applicants who are currently in full time studies | Only students in their final year of studies are eligible for the programme. However, if you currently hold a job, you will not be eligible, as per treatment of case #1. | No |

| 8 | Applicants who are currently in part time studies | Yes, if you can be full time committed to the Venture Building programme. | Yes |

| 9 | Applicants who are still studying and on scholarship that requires them to serve a bond after graduation | No | No |

| Others | |||

| 10 | Applicants who have attended any SGUnited Traineeship or SGUnited Skills Programmes | No | No |

| 11 | Applicants who have previously joined other Venture Building programmes (incl. commercial VB programmes) | No | No |

Under the “Start” track scheme, teams of entrepreneurs with innovative business ideas can approach any Enterprise Singapore-appointed Accredited Mentor Partners (AMP) with their innovative business ideas. The AMPs will identify and recommend qualifying applicants for funding support based on the uniqueness of business concept, feasibility of business model, strength of management team, and potential market value. Upon successful application, the AMP will assist the startups with advice, learning programs and networking contacts. Enterprise Singapore will also provide the startups with a startup capital grant of $50,000. Startups are required to raise and commit S$10,000 as co-matching fund to the grant.

Applicants will need to reach out to an Accredited Mentor Partners (AMP) of choice and submit their pitch deck for the AMP’s consideration. AMP will assess applicants based on (but not limited to) the following criteria:

If the AMP assesses that the applicant has met the eligibility and evaluation criteria, they will provide a letter of recommendation to the applicant. Applicants must then attach this letter in an online application form to be submitted to Enterprise Singapore within 2 weeks from the receipt of the letter of recommendation. Enterprise Singapore will inform the applicant and AMP on the application status for the grant.

The grant is open to all Singaporeans/Permanent Residents who meet the following conditions at the time of application:

The enhancements will take effect on 25 Sep 2020. Any applications received by ESG prior to this date will follow the current Startup SG Founder grant conditions, which include:

i. Grant amount of $30,000 over a 12-month period

ii. Co-matching ratio of 1:3 (ie. Founder(s) must raise $10,000 in capital)

iii. Only one main applicant required

Any applications received by ESG from 25 Sep 2020 onwards will follow the new Startup SG Founder grant conditions, (refer to Para 2.ii). Some key conditions include:

i. Increased grant amount of $50,000 over a 12-month period

ii. Reduced co-matching ratio of 1:5 (ie. co-investment of $10,000 required)

iii. Minimum 3 SC/PR employees (including the founder), two of whom must be first-time founders.

If the AMP wishes to recommend the application, the AMP will decide on appropriate milestones together with the applicant(s). The AMP’s recommended application and milestones will then be surfaced to ESG for vetting and approval. The grant will be disbursed in 2 tranches based on agreed project milestones. You will have up to 12 months from the date of letter of offer to meet the milestones to draw down on the grant.

ESG continuously reviews all our programmes including the Startup SG Founder and its appointed AMPs. Any further enhancements will be subject to a review in FY2021. In addition, there are various forms of Startup SG support catered to different stages of startups, e.g. Startup SG Equity and Startup SG Tech schemes. The National Innovation Challenges were also recently launched to spur demand from companies and government agencies for innovative solutions by startups.

Pursuing entrepreneurship in this time is challenging. But the Government is providing various forms of support to mitigate this risk.

a. The enhancement of Startup SG Founder programme is example. Startups under our Startup SG Founder scheme are closely supported and mentored by ESGappointed AMPs, who provide useful resources, coaching and networks for startups and entrepreneurs to tap on. There is also significant support from government effort and community-led initiatives to help the local startup ecosystem, to mitigate risks in pursuing entrepreneurship during this time.

b. In June 2020, the Special Situation Fund of S$285 million was launched to support promising startups with strong growth potential to continue with innovation and product development in Singapore.

c. The Startup SG Equity scheme was enhanced earlier this year with an additional S$300 million to catalyse more investments into Singapore-based deep-tech startups. Both are done through co-investments with the private sector. Several ecosystem partners have also stepped up to provide mentorship virtually to startups on a pro bono basis. For example, community builders AngelCentral and Found8 launched online sites that list tips and advisories for any startups during this tough time. VCs such as Antler also launched a call to invest in early-stage startups with solutions to tackle COVID-19. It will invest up to US$500,000 by this year in such startups, with the aim to generate more innovative solutions from startups to solve immediate challenges relating to the current pandemic crisis.

No. Startup founders who have ready business plans and do not require entrepreneurial training can continue to apply to any existing AMPs to be considered for the Startup SG Founder grant. The introduction of the “Train” track merely offers more support for entrepreneurs who wish to get training and advices for market validation of their business ideas before launching their startups.

If you would like to explore the various support available for startups, you may find it helpful to check out the Startup SG website (www.startupsg.gov.sg) or to make an appointment with one of the SME centres (https://partnersengage.enterprisesg.gov.sg/book-appointment). The business advisors will advise you more on the appropriate schemes and assistance for your business. ESG is unable to vet through or give comments on the business proposal, as ESG can only evaluate grant applications submitted in accordance to the stated requirements of the programme.

Click here for more Startup SG Founder FAQ.

In the Ministerial Statement made by DPM Heng Swee Keat on Mon, 5 Oct 2020, he stated that there will be an extended and enhanced support for firms and workers.

Companies looking to grow their businesses, increase productivity or expand overseas will soon be able to tap bigger grants and expanded loan schemes. These moves will provide more support for businesses during the Covid-19 pandemic and help them to transform, Trade and Industry Minister Chan Chun Sing said as he announced the enhancements to several grant and loan schemes on Monday, Oct 12.

This grant provides Small and Medium Enterprises (SMEs) with financial assistance to help take your business overseas. You will be rewarded a maximum of 2 MRA grants for each fiscal year. To be eligible for this grant, you need to:

Up to 70 per cent of qualifying costs, including identifying business partners and setting up overseas.

Up to 80 per cent of qualifying costs from 1 Nov 2020 to 30 Sept 2021. Will also cover participation in virtual trade fairs from 1 Nov 2020.

The Enterprise Development Grant helps Singapore companies grow and transform. This grant funds qualifying project costs namely third party consultancy fees, software and equipment, and internal manpower cost. To qualify for this grant, you need to:

Up to 80 per cent of qualifying costs until 31 Dec 2020.

Higher support of up to 80 per cent extended by nine months to 30 Sept 2021, after which it will revert to up to 70 per cent.

The Productivity Solutions Grant (PSG) supports companies keen on adopting IT solutions and equipment to enhance business processes.

For a start, PSG covers sector-specific solutions including the retail, food, logistics, precision engineering, construction and landscaping industries. Other than sector-specific solutions, PSG also supports adoption of solutions that cut across industries, such as in areas of customer management, data analytics, financial management and inventory tracking.

To help enterprise implement COVID-19 business continuity measures, the scope of generic solutions has expanded to include:

SMEs can apply for PSG if they meet the following criteria:

Up to 80 per cent of qualifying costs until 31 Dec 2020.

Higher support of up to 80 per cent extended by nine months to 30 Sept 2021, after which it will revert to up to 70 per cent.

The Temporary Bridging Loan Programme (TBLP) allows eligible enterprises to borrow up to S$5 million, with a repayment period of up to 5 years.

Under the scheme, interest rates charged by Participating Financial Institutions (PFIs) are capped at a maximum interest rate of 5% per annum.

To be eligible for TBLP, you need to:

Loans of up to $5 million, with up to 90 per cent risk-sharing by the Government until 31 March 2021.

Loans of up to $3 million, with up to 70 per cent risk-sharing by the Government from 1 April to 30 Sept 2021.

This programme helps enterprises finance the fulfillment of secured overseas projects.

The supportable loan types include:

To be eligible for this loan, you are:

You need to:

Loans of up to $50 million for secured overseas projects, with at least 50 per cent risk-sharing by the Government.

Expanded to allow construction companies to take up loans of up to $30 million for secured domestic projects, with at least 50 per cent risk-sharing by the Government, starting from 1 Jan 2021.

Finance trade needs, including:

Eligibility:

Loans of up to $10 million, with up to 90 per cent risk-sharing by the Government until 31 March 2021.

Loans of up to $10 million, with up to 70 per cent risk-sharing by the Government from 1 April to 30 Sept 2021.

The government will extend the Enhanced Training Support Package (ETSP) which was enhanced in the Resilience Budget, for another six months, until 30 June 2021 to provide enhanced course fee subsidies for firms in our hardest-hit sectors. DPM Heng also said that he will extend the ETSP to the Marine and Offshore sector from 5 Oct 2020, on top of the existing sectors such as Air Transport, Retail, and Tourism. In recognition of the gradually recovering economic situation, we will also be lowering the absentee payroll rates to 80% from January 2021, capped at $7.50 per hour.

In tandem, the government will continue to provide strong support to firms that are growing by:

As persons with disabilities may face greater challenges in finding jobs, the government will provide the higher tier of wage support of 50% under the JGI to all Persons with Disabilities.

This will apply to new hires of Persons with Disabilities from September 2020 to February 2021.

To give a boost to businesses seeking to internationalise, transform and digitalise, there will be an extension or enhancement to the capability-building grants:

These will enable firms to tap on new sources of growth. MTI will announce details in the coming weeks.

Under the rental relief framework, a landlord who is unable to reach an agreement with is tenant may apply to have an independent rental relief ascertain:

a) The tenant’s eligibility for rental waivers (either the portion supported by Government assistance, and/or the portion borne by the landlord)

b) The landlord’s eligibility to provide a reduced amount of rental waivers, on the basis of financial hardship

The amendments to the Act proposed on September 3, will expand the powers of rental relief assessors so that they can make determinations on unresolved disputes relating to the amount of rent to be waived under the framework, where the amount is affected by any of the following factors:

a) The amount of maintenance and service charges, especially where such charges are not explicitly listed in the lease or license agreement

b) The amount that can be offset by assistance provided by the landlord earlier

c) The tenant is occupying the property for only a part of the relief period

d) There are multiple-sub tenants in the same property

The amendment Bill will also clarify the existing Part 8 of the Act – not yet in force – that allows parties of some contracts to get relief if they are affected by breaches or delays in construction, supply or related contracts.

It will specify that no application for relief for such contracts can be filed if court, arbitral or Building and Construction Industry Security of Payment Act (Sopa) proceedings related to the application have already started.

Conversely, once an application for relief ha been filed, the other parties of the contract cannot commence, arbitral or Sopa proceedings or the same matter, until a determination is made or the application is rejected or withdraw.

If a determination is made and the terms of the contract are adjusted, any subsequent applications and determinations made under Sopa must be based on the adjusted contract terms.

In cases where a Sopa application is made before the other party seeks relief under the Act, the Sopa adjudicator will have powers to grant relief – similar to that of the assessors – to account for the impact of Covid-19.